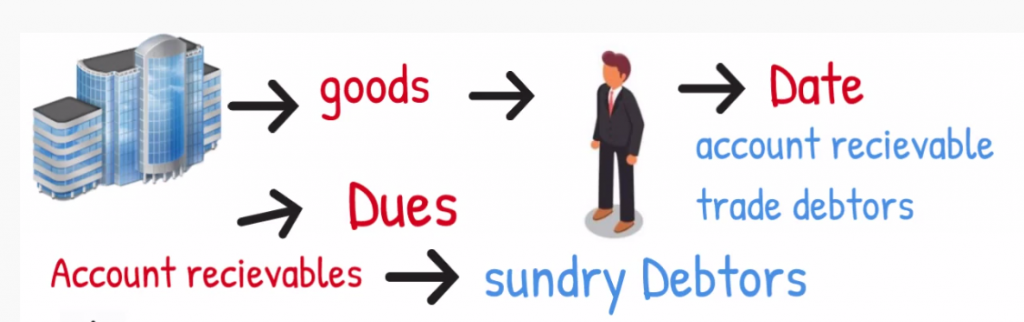

好吧,卖东西卖服务,开出发票,要求对方30天内支付。就是 trade debtors/account recievalbe 。

生意就是现金流,30天后能收到的现金就是trade debtors/account recievable/sundry debtors。

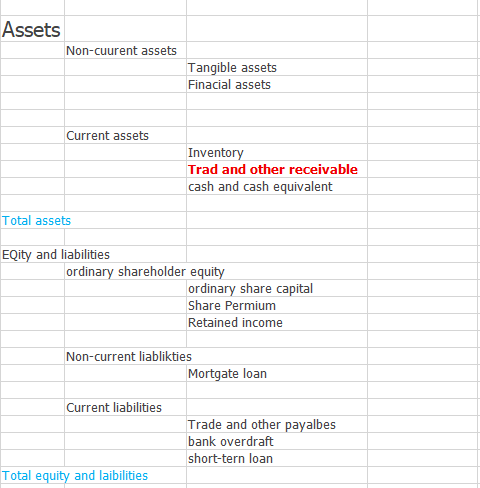

会计等式accounting equation

资产assets=负债liabilities+所有者权益owners‘ equity

是客户欠咱们公司钱!在资产负债表balancesheet什么位置呢?

trade debtors/account recievable/sundry debtors,是资产,是Current assets(流动性资产)。

流动性资产current包括现金cash和预期在资产负债表balance sheet日期后12个月内转为现金或消费consumed的资产assets。

客户答应30天后支付就是trade debtors/account recievable/sundry debtors。是小于12个月,就能成为宝贵的现金流的。

流动性资产current assets中:

- 第一位是现金cash,现金分银行账面上的current account上的balance,和手持的现金cash on hand

- 下面的三个资产assets都是在12个月内应转化为现金或被消费的资产,分别是:应收帐款Accounts receivable,即客户应该付给公司的钱;商品库存Merchandise inventory,即可以售卖的货物;预付开支Prepaid expenses,比如提前付的房租。

非流动性资产non-current assets:

土地land,仓库warehouse building,货车Van,商店的固定装置Store fixtures,特许经营费/加盟费Franchise fee,都是期望产生超过一年(从盈亏平衡表的日期往后算)的经济价值的。

非流动性资产non-current assets中的有些有形资产tangible assets比如仓库warehouse building有相关的资产备抵账户/资产对冲contra-asset account,叫累计折旧accumulated depreciation,减少了资产assets的价值。

留存收益retained earnings/retained income代表了实体entity迄今to date累计的收入cumulative earning,减去less该利润分配distribution of earnings给该实体entity所有者的任何收益。

资产负债表距今已有将近500年的历史了,从意大利的路卡帕乔利就开始有了。

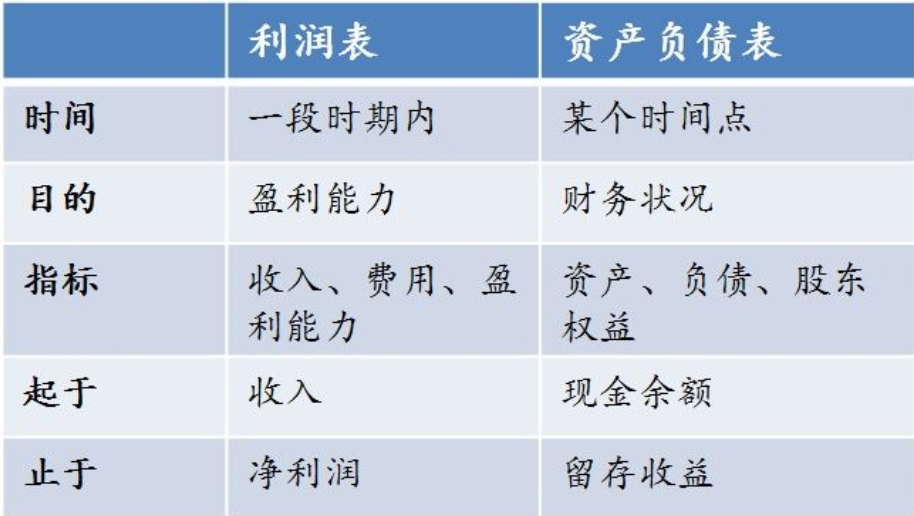

在某个特定时点上,公司有多少钱(表现为资产),欠别人多少钱(表现为负债),值多少钱(表现为股权),即: 资产=负债+股权,反映公司在给定时间点上的财务状况。

什么叫利润表?

利润表其实体现的就是资产负债表里面的一个科目,叫做未分配利润的变动情况;利润来源于收入,收入减去成本费用,就得到利润。这就是利润表的基本。反映公司在给定时间段内的经营成果。

举个例子,假设一家企业从同一年开始经营,收入一亿元、费用八千万元、净利润两千万元。且企业要求款到交货,现金流畅。

现金流量表

现金流量表为会计的资产负债表提供的是 现金的期初余额opening balance和现金的期末余额ending balance

利润表

为资产负债表retained earning科目提供期初余额和期末余额。

开始时间点的留存收益retained earnings余额beginning balance+净收入/亏损net income/loss-股息dividends=结束时间点的留存收益retained earnings余额ending balance股利dividends是对所有者收益owners‘ equity的分配distribution,通常以现金cash的形式。 股息dividends的支付减少了留存收益retained earnings账户。总而言之,有两个事件会在一个会计期间during an accounting period内更改留存收益科目retained earnings account。首先,实体entity在此期间获得的净收入(亏损)Net Income (loss)增加(减少)了留存收益科目retained earnings account。其次,在此期间支付的任何股息dividends(分配给投资者的股息)都会减少留存收益科目retained earnings account。股利dividends的支付不是一种费用expense;它是向投资者分配股权资本equity capital。 因此,股利dividends的支付不记入损益表income statements;相反,它直接减少留存收益账户retained earnings account。

毛利gross income=sales-sales cost

gross income-operating expenses(marketing/selling/administrative expense)=operating income

income before tax=operating income-interest expenses

net income=income before tax-tax expenses(corporation tax)

net income和dividens会影响 retained earning account

dividens 不是费用,不计入损益表,不计入损益表profit and loss,直接减少retained earnings account

Comments are closed, but trackbacks and pingbacks are open.